By Jenny Kiffmeyer, J.D – The Retirement Learning Center

When might a cash balance plan be a good fit?

ERISA consultants at the Retirement Learning Center (RLC) Resource Desk regularly receive calls from financial advisors on a broad array of technical topics related to IRAs, qualified retirement plans and other types of retirement savings and income plans, including nonqualified plans, stock options, and Social Security and Medicare. We bring Case of the Week to you to highlight the most relevant topics affecting your business.

A recent call with an advisor in New Mexico is representative of a common question related to maximizing retirement plan contributions. The advisor asked: “How can I determine if a cash balance plan might be a good fit for a business owner?”

Highlights of Discussion

The question of whether to set up a qualified retirement plan has important tax ramifications. Therefore, business owners would be best served by seeking the guidance of a tax professional when making such a decision.

As a type of defined benefit plan, a cash balance plan requires an adopting employer to fund the plan to provide participants with a promised retirement benefit. Cash balance plans are most popular among smaller, well-established firms that have significant and consistent cash flow (e.g., law firms, medical groups, and professional firms such as CPAs, architects, and consultants). They also work well for older small business owners who are no longer making heavy investments in their businesses, and have significant amounts of pass-through income, resulting in high tax bills.

To determine suitability for a cash balance plan, consider the following questions. The more “yes” responses the greater the possibility a business could benefit from having a cash balance plan.

| Question | Yes | No | Why it Matters |

|---|---|---|---|

| 1. Is the business owner over age 50? | The potential to contribute more income to a cash balance plan increases with age. | ||

| 2. Does the business owner have less of a need to reinvest in the business? | If the owner has put money into the business in prior years, the business is now, likely, well established, freeing up capital. | ||

| 3. Does the owner have significant pass-through income? | This can lead to discussions on how to reduce a large tax bill. | ||

| 4. Does the owner want to catch-up on saving more for the future? | Cash balance plans allow for higher contribution and deduction limits than defined contribution plans. | ||

| 5. Has the business owner shown interest in setting up a nonqualified deferred compensation plan (NQDC) to save more? | NQDC plans do not reduce taxable income for business owners of pass-through entities. | ||

| 6. Has the business owner shied away from a define benefit plan due to complexity and employee coverage issues? | Cash balance plans are less complicated to maintain than traditional defined benefit plans, and design features allow owners to maximize contributions for themselves. |

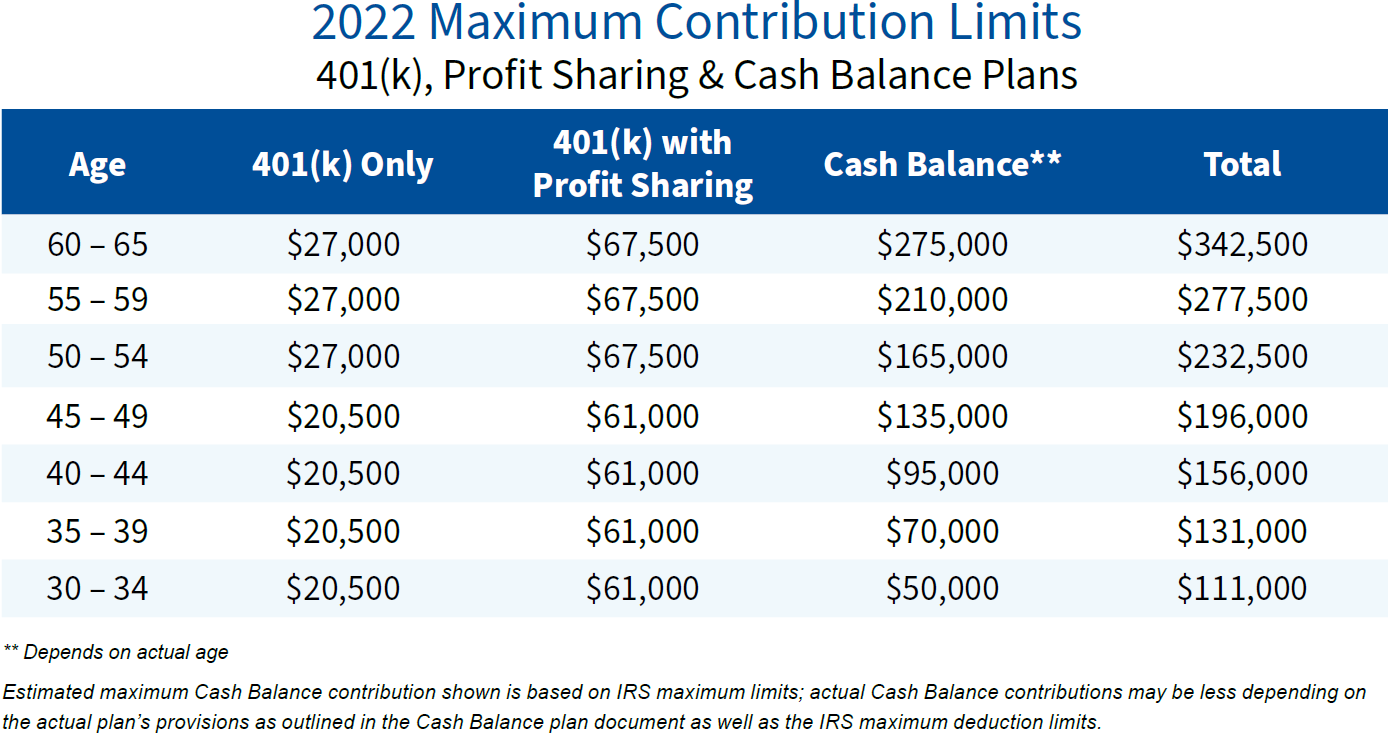

As the table below illustrates, cash balance plans can allow much higher levels of contributions than a profit sharing or 401(k) plan. That equates to higher tax deductions for business owners. For some businesses, having both a defined contribution and cash balance plan may be appealing.

Conclusion

There are some key characteristics to look for in a business owner when evaluating whether a cash balance plan might be a good fit. For the right candidate, a cash balance plan—or even a combination cash balance and defined contribution plan—can provide significant benefits. Above all, whether to set up a qualified retirement plan is an important tax-related question that a business owner should only answer with the help of his or her tax professional.

Click here to learn more about Cash Balance Plans.