By Jenny Kiffmeyer, J.D – The Retirement Learning Center

Filing Form 5500 Without an Audit Report

ERISA consultants at the Retirement Learning Center Resource Desk regularly receive calls from financial advisors on a broad array of technical topics related to IRAs, qualified retirement plans and other types of retirement savings plans, including nonqualified plans. We bring Case of the Week to you to highlight the most relevant topics affecting your business.

A recent call with a financial advisor from West Virginia involved filing a Form 5500, Annual Return/Report of Employee Benefit Plan. The advisor asked: “My client is afraid the audit report for his 401(k) plan will not be complete by the October 15th extended filing deadline. Can he file Form 5500 without the audit report by the deadline, and provide the audit report later?”

Highlights of Discussion

The Department of Labor’s (DOL’s) EFAST2 electronic system will accept a Form 5500 filing without the independent qualified public accountant (IQPA) audit report attached, however the DOL will treat the submission as an “incomplete filing and [it] may be subject to further review, correspondence, rejection, and assessment of civil penalties” (see Q&A 25 of FAQs on EFAST2 Electronic Filing System).

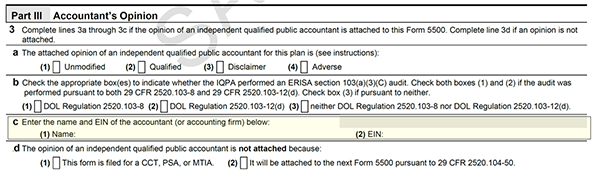

The guidance goes on to state that filers must correctly complete Schedule H, Part III, line 3 regarding the plan’s IQPA report. That means your client will only be able to fill in the information on 3(c) Name and EIN of the IQPA. Lines 3(a), (b) and (d) would not apply in this case and must be left blank. If your client files Form 5500 without the required IQPA report, he or she should correct that error as soon as possible.

Excerpt from Schedule H, Form 5500

Without the required IQPA report, the filing is incomplete and the DOL may (and likely will) reject the filing pursuant to ERISA Sec. 104(a)(5). If your client receives an official rejection letter or notice from the DOL, he or she has 45 days to resubmit the filing correctly [see ERISA Sec. 104(a)(5)] . Failure to submit a corrected filing allows the DOL to issue a notice of intent to assess a penalty. Note, there is a 30-day grace period to ask for waiver of the penalty due to reasonable cause [DOL Regulation 2560.502c-2(b) & (e)].

The DOL can assess a penalty of up to $2,400 a day for each day a plan administrator fails or refuses to file a complete report (ERISA Sec. 502(c)(2) and DOL Reg. 2560.502c-2). The IRS may separately assess penalties per the SECURE Act, effective for returns due after December 31, 2019, the IRS late fees are $250 per day up to $150,000. Both agencies could waive or abate those penalties if the plan sponsor can establish “reasonable cause” for the late filing.

The DOL’s Delinquent Filer Voluntary Compliance Program (DFVCP) encourages voluntary compliance with Form 5500 filing requirements and gives delinquent plan administrators a way to avoid higher civil penalty assessments by satisfying the program’s requirements and voluntarily paying a reduced penalty. Eligibility for the DFVCP is limited to plan administrators who have not been notified in writing by the DOL of a failure to file.

Conclusion

The DOL will accept a Form 5500 filing without the IQPA audit report attached, however the agency will treat the submission as an incomplete filing, subject to penalties if not timely corrected and resubmitted.