By Jenny Kiffmeyer, J.D – The Retirement Learning Center

Plan Contributions for 403(b) and Governmental 457(b) Plans

ERISA consultants at the Retirement Learning Center Resource Desk regularly receive calls from financial advisors on a broad array of technical topics related to IRAs, qualified retirement plans and other types of retirement savings plans, including nonqualified plans. We bring Case of the Week to you to highlight the most relevant topics affecting your business.

A recent call with a financial advisor from Illinois is representative of a common inquiry related to the maximum annual limit on employee salary deferrals. The advisor asked: “One of my clients participates a 403(b) plan and a governmental 457(b) plan (through a state university). Her accountant is telling her that she, potentially, could contribute $41,000 of deferrals between the two plans for 2022. How can that be so?”

Highlights of Discussion

Generally speaking, it may be possible for her to contribute more than one would expect given the plan types she has and based on existing plan contributions rules, which are covered in the following paragraphs. Your client should rely on her tax advisor in order to determine what amounts she can contribute to her employer-sponsored retirement plans because this is an important tax question that is best answered with the help of professionals.

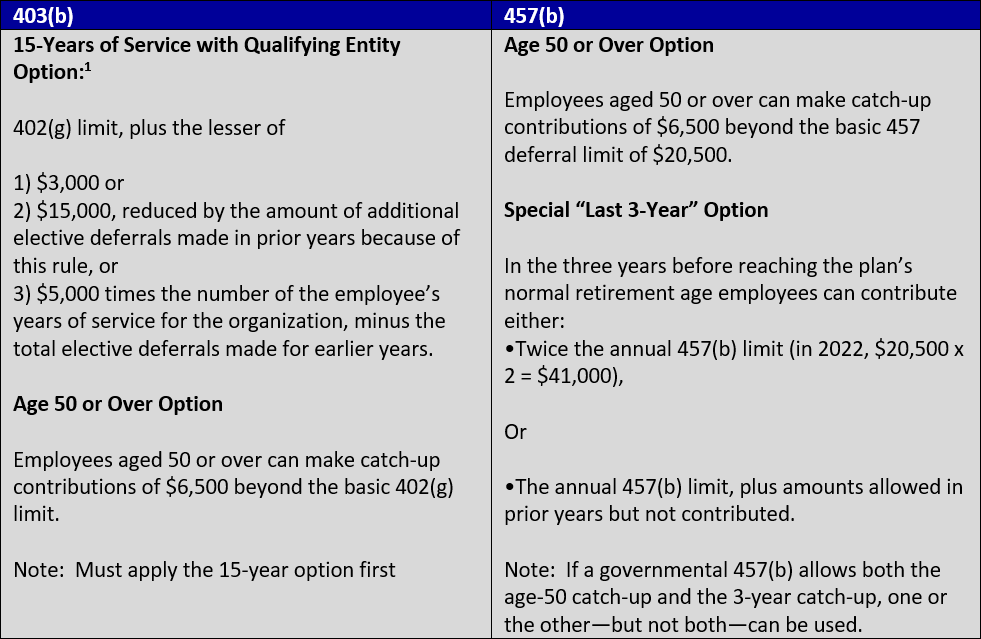

For 2022, 457(b) contributions (consisting of employee salary deferrals and/or employer contributions combined) cannot exceed $20,500, plus catch-up contribution amounts ($6,500) if eligible [Treasury Regulation Section (Treas. Reg. §1.457-5)]. Since 2002, contributions to 457(b) plans no longer reduce the amount of deferrals to other salary deferral plans, such as 401(k) or 403(b) plans. A participant’s 457(b) contributions need only be combined with contributions to other 457(b) plans when applying the annual contribution limit. Therefore, contributions to a governmental 457(b) plan are not aggregated with deferrals an individual makes to other types of deferral plans.

Consequently, an individual who participates in both a governmental 457(b) plan and one or more other deferral-type plans, such as a 403(b), 401(k), salary reduction simplified employee pension plan, or savings incentive match plan for employees has two separate annual deferral limits. Here’s an example.

Example:

For 2022, 32-year-old Toni is on the faculty at the local state university and participates in its 457(b) and 403(b) plans. Assuming adequate levels of compensation, Toni can defer up to $20,500 in her 403(b) plan, plus another $20,500 to her 457(b) plan—for a total of $41,000.

Also, keep in mind the various special catch-up contribution options depending on the type of plan outlined next.

Another consideration when an individual participates in more than one plan is the annual additions limit under IRC Sec. 415(c),[2] which typically limits plan contributions (employer plus employee contributions for the person) for a limitation year [3] made on behalf of an individual to all plans maintained by the same employer. However, contributions to 457(b) plans are not included in a person’s annual additions (see 1.415(c)-1(a)(2).

[1] A public or private school, hospital, home health service agency, health and welfare service agency, church, or convention or association of churches (or associated organization) and it is allowed by the terms of the plan document.

[2] For 2022, the limit is 100% of compensation up to $61,000 (or $67,500 for those > age 50).

[3] Generally, the calendar year, unless the plan specifies otherwise.

Conclusion

Sometimes individuals who are lucky enough to participate in multiple employer-sponsored retirement plan types may be puzzled by what their maximum contribution limits are. This is especially true when a person participates in a 403(b) and 457(b) plan. That is why it is important to work with a financial and/or tax professional to help determine the optimal amount based on the participant’s unique situation.